- Solutions

- Pricing

78% of consumers would continue using their bank if they received personalized support, but just 44% of banks are actually delivering it. It’s a gap wide enough for any competitor to slide in.

And if you compare sectors, industries like retail and travel, where stakes are dramatically lower, understand customer journeys way better than banks, NBFCs, or wealth firms who manage people’s life savings.

The finance industry is sitting on more customer data than almost any other sector. But still struggles when it comes to delivering a smooth customer experience.

That’s where a modern CRM for financial services industry actually matters.

Let’s start with the simple reality:

Financial services run on relationships, but scale runs on systems.

The moment your customer base grows beyond a few thousand, relationship management can’t stay manual. And you already know how complex this ecosystem is:

Banks deal with onboarding, KYC, risk checks, and multi-product cross-sell.

Lending companies juggle field teams, loan origination, approvals, and collections.

Wealth firms handle portfolios, advisory pipelines, risk profiling, and compliance calls.

None of these workflows can be handled in spreadsheets or outdated CRMs that require heavy configuration.

Here’s where most generic CRM tools fail.

A banking customer doesn’t have a straightforward A→B→C journey.

It’s more like:

A → B → B1 → C → back to A → D → A again → renewal → upsell → advisory → audit → compliance check → service reroute.

It’s a loop.

Let’s break down how this journey behaves across sectors.

A typical retail banking journey looks like:

Lead captured

Pre-KYC

Video KYC

Risk scoring

Product match (savings, credit card, personal loan, insurance)

Multi-team handoffs

Approval

Service management

Inside each block, there are 3–10 micro-steps.

And every micro-step has compliance obligations.

This is exactly why banks were early adopters of CRM tools. But adoption doesn’t mean effectiveness.

The problem:

Legacy CRMs demand the bank adjust their internal workflows to the software’s structure, not the other way around.

Modern CRMs flip that logic.

And this is where CodeBlox quietly fits in: instead of using a rigid CRM template, banks can literally map their own internal journey (KYC flow, approvals, escalations, DSAs, RM workflows) with drag-and-drop. No drama. Just building the journey the way they want.

Lending has a different complexity.

Agents are in the field.

Documents are half-digital, half-physical.

Approvals move through multiple levels.

Risk scores update at every step.

And then… collections.

Ideally, a crm finance industry workflow for lending should cover:

But most CRMs don’t offer even half of this natively.

So lenders end up with 5 different systems:

CRM + LOS + LMS + Collections system + Field app.

Modern platforms are now allowing lenders to unify this entire pipeline into one mapped journey.

Not as a “template,” but as a workflow you design yourself.

That’s a huge shift in the industry.

Wealth management has fewer customers but deeper relationships. Hence, a CRM for wealth firms must support:

Relationship hierarchies (family accounts, HNI structures)

Old CRMs were not built for this level of nuance. And that’s why the wealth sector has been rapidly shifting toward customizable CRM frameworks.

Every financial institution ultimately wants only four things:

If a CRM doesn’t enable these outcomes, everything else is decoration. Let’s break the real capabilities that matter.

A CRM should show:

Pretty basic, but 80% of finance CRMs don’t show this level of clarity.

With modern workflow builders like CodeBlox, this journey mapping becomes visual, editable, and aligned with how you work.

Instead of the CRM telling you “lead → qualify → convert,” you tell the CRM “this is our exact compliance flow.”

Banking and finance have the highest regulatory burden and there is no scope of manual compliance tracking.

Automated reminders for renewals (KYC refresh, portfolio reviews, loan NPA stages)

This is where no-code customization becomes non-negotiable.

As finance regulations are updated faster than tech teams can code, you need a system where compliance can be drag-and-dropped into every workflow.

Real segmentation in finance is behavior + portfolio + risk + engagement.

Examples:

Real automation for finance includes:

Teams work in silos and have no update on what other teams are currently working on. A CRM must connect these teams.

Every stakeholder should see their part of the journey. This is exactly where rigid CRMs collapse and they can’t handle multi-team parallel operations.

But workflow-centric CRMs or no-code stacks like CodeBlox adapt much better.

Especially for lending and insurance mobile CRMs should allow:

Financial services don’t need 200-page reports.

They need:

You don’t need to buy a CRM template for finance.

Most institutions today prefer creating their own workflows, their own LOS, LMS, KYC flow, advisory flow, or collections pipeline. All these without writing code.

That’s where CodeBlox quietly enters the narrative.

Institutions simply:

The result feels like a CRM built just for them. This is why the no-code movement is gaining momentum in BFSI.

{CTA button:Explore CodeBlox:https://www.codeblox.com/solutions/no-code:<h3>Want to know more about the no code platform CodeBlox?</h3>}

Not all CRMs are built equal. Finance teams typically encounter four categories. Let’s break them down without the usual vendor jargon.

These are the usual sales CRMs. They are fine for traditional pipelines but awful for BFSI because:

❌They don’t understand compliance

❌They don’t map multi-stage approval flows

❌They have rigid data structures

❌They assume every deal has a single owner

❌They treat documents as attachments, not compliance checkpoints

These tools come with prebuilt finance modules. They work, but they often feel like you are buying a pre-constructed house.

The moment a bank wants to tweak even one flow, it becomes a custom development project. This is where teams get frustrated as changes takes long till it can be used.

Loan Origination + Loan Management solutions are powerful. But many vendors now market them as complete CRMs. They are not. You will still need a separate CRM layer, which leads to duplicate data.

This is where the industry is shifting. Instead of adjusting your institution to a CRM template, no-code platforms allow you to build your own CRM, including:

Exactly how your organization works — not how software vendors assume you work. This category solves the rigidity problem without forcing custom coding.

When we talk about CRM for financial services industry, we are really talking about systems that do more than just track contacts and sales. CodeBlox is a cloud-based, no-code business application platform that empowers teams to build powerful custom systems, including CRM workflow,s without writing any code. It is designed to support complex, real-world business processes while offering the flexibility to adapt them over time.

Here’s how CodeBlox helps institutions build CRM capabilities that actually work for banking, lending, and wealth workflows:

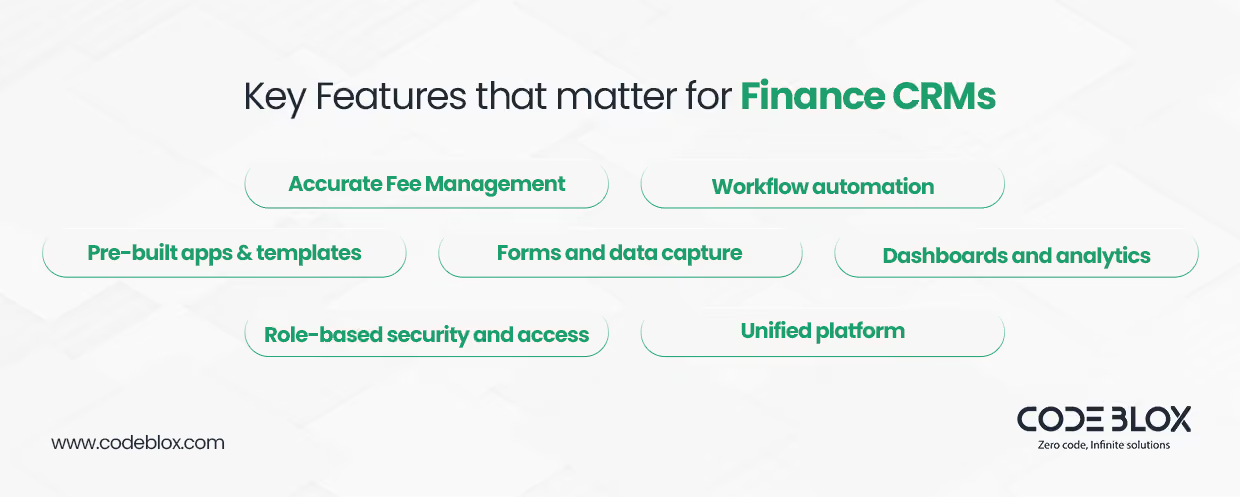

1. Drag-and-drop application builder

CodeBlox’s visual design center allows teams to create fully customized business applications, including screens, forms, dashboards, and workflows. This means you can build CRM modules based on your finance processes.

2. Workflow automation

You can visually define everything from when a new lead enters the system to how onboarding or compliance checklists progress. Workflow automation reduces manual steps and improves consistency across the customer journey.

3. Pre-built apps & templates

CodeBlox includes pre-built templates that can be used as starting points and customized further. This accelerates development and lets teams iterate quickly.

4. Forms and data capture

Users can create custom forms with extensive data types, validations, conditional fields, and linked records. This is important for finance workflows such as KYC, lead qualification, loan data, and client profiles.

5. Dashboards and analytics

With drag-and-drop analytics, teams can visualize key metrics from conversion rates and approval bottlenecks to portfolio performance and service queues in real time. This helps decision makers see where journeys break and what needs fixing.

6. Role-based security and access

CodeBlox supports granular access control, so different roles (like RMs, credit officers, compliance reviewers) have access to only the data they would need and not everything. This is critical in finance, where data confidentiality and audit trails are non-negotiable.

7. Unified platform

Instead of stitching together multiple tools or systems, CodeBlox lets you run business processes from a common database and dashboard, which reduces data silos and increases operational clarity.

If the customer journey is broken, nothing else matters. A mapped, automated, compliance-ready CRM removes friction across banking, lending, and wealth workflows — and that’s where institutions see the real lift: higher conversion, cleaner execution, faster decisions, fewer errors.

The future belongs to BFSI teams that design their own workflows and let technology follow, not dictate. That’s the advantage modern platforms like CodeBlox unlock.

{CTA button:Schedule a demo:https://www.codeblox.com/schedule-demo:<h3>If you would like a walkthrough of how CodeBlox can align with your internal finance processes, you can schedule a session with the team and review it together.</h3>}

Find answers to the most common questions about our no-code platform and how it can help you build powerful business application solutions without writing a single line of code.

Yes, because institutions can build banking, lending, or wealth workflows exactly as they operate internally. No rigid templates. No dependency on vendors. With easy drag and drop, institutions can create workflows as per their requirements.

For lending: faster KYC, smart routing, field-visit tracking, auto-collections workflows.

For wealth: portfolio review cycles, advisory notes, risk profiling, client segmentation.

In both cases, CRM removes friction and makes every step predictable.

Because LOS/LMS/core systems handle transactions and not relationships. A crm finance industry stack connects the entire customer lifecycle: onboarding → risk → service → renewal → upsell → collections, giving teams visibility they don’t get anywhere else.

It must support KYC workflows, role-based approvals, document validation, field operations, advisory scheduling, portfolio tracking, automation, and a unified customer profile. Finance workflows are multi-team and high-compliance, which generic CRMs can’t handle.

A finance CRM maps every step so that institutions can see exactly where customers drop off and fix those gaps. It aligns sales, credit, ops, and compliance into one connected journey.